Asset Beta vs. Equity Beta

When analyzing a company's risk, investors and analysts often use beta to measure its volatility relative to the market. However, there are two types of beta: Asset Beta (Unlevered Beta) and Equity Beta (Levered Beta). Understanding their differences is crucial for making informed investment decisions.

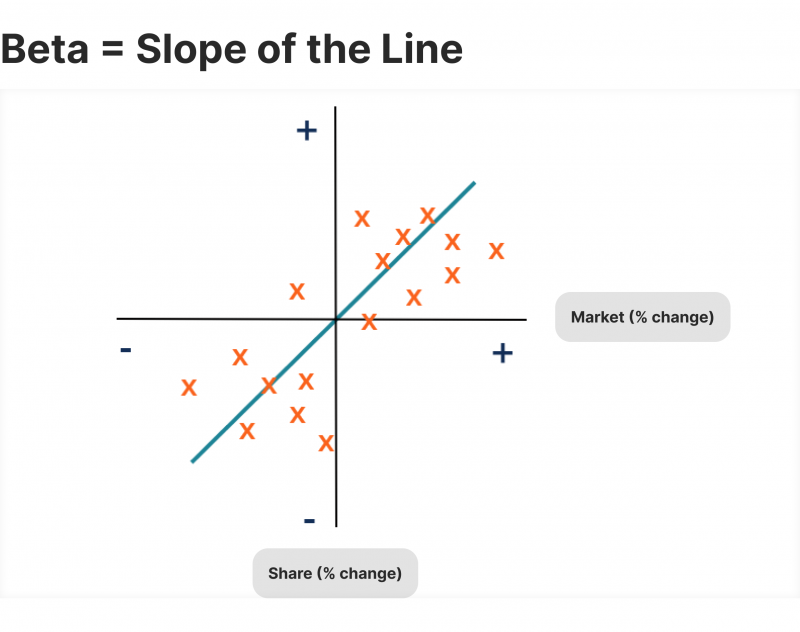

What is Beta in Finance?

Beta measures a stock's sensitivity to market movements.

- Beta > 1 → The stock is more volatile than the market.

- Beta < 1 → The stock is less volatile than the market.

- Beta = 1 → The stock moves in line with the market.

But when evaluating a company’s true risk, it’s important to distinguish between Asset Beta and Equity Beta.

What is Asset Beta (Unlevered Beta)?

Asset Beta measures a company's risk without the impact of debt. It represents the risk of the company’s core business operations, independent of its capital structure.

Formula:

Asset Beta = Equity Beta / (1+(1−Tax Rate)×Debt/Equity)

What is Equity Beta (Levered Beta)?

Equity Beta measures the risk of a stock considering the company’s debt. It reflects both business risk and financial risk (due to leverage).

Formula:

Equity Beta = Asset Beta × (1 + (1 − Tax Rate) × Debt/Equity)

Key Differences

1) Definition:

- Asset Beta (Unlevered Beta): Measures business risk without considering debt.

- Equity Beta (Levered Beta): Measures total risk, including the impact of debt.

2) Impact of Debt:

- Asset Beta: Ignores debt and reflects pure business risk.

- Equity Beta: Includes the effect of leverage, making it higher for companies with more debt.

3) Use Case:

- Asset Beta: Used for industry comparisons and risk assessment, as it removes financing structure differences.

- Equity Beta: Used in the Capital Asset Pricing Model (CAPM) to calculate the cost of equity.

4) Sensitivity to Market:

- Asset Beta: Less sensitive to market movements since it excludes leverage risk.

- Equity Beta: More sensitive to market fluctuations, especially for highly leveraged companies.

5) Who Uses It?

- Asset Beta: Analysts comparing companies within the same industry.

- Equity Beta: Investors assessing stock risk and expected returns.

Example

Assume a company has:

- Equity Beta = 1.5

- Debt/Equity Ratio = 0.5

- Tax Rate = 30%

Step 1: Calculate Asset Beta

Asset Beta = 1.5 / (1+(1−0.3)×0.5)

= 1.5 / (1+0.35)

= 1.5 / 1.35

= 1.11

Step 2: Recalculate Equity Beta (if needed)

Equity Beta = 1.11 × (1+(1−0.3)×0.5)

= 1.5

This shows how debt increases Equity Beta, making the stock riskier for investors.

When to Use Asset Beta vs. Equity Beta?

a) Use Asset Beta when:

- Comparing companies in the same industry without leverage effects.

- Assessing pure business risk.

- Valuing private firms or divisions of a company.

b) Use Equity Beta when:

- Estimating the cost of equity using the CAPM model.

- Evaluating a company’s stock risk for investors.

- Analyzing firms with different debt levels.

Conclusion

Both Asset Beta and Equity Beta are important in financial analysis. Asset Beta isolates business risk, while Equity Beta includes the impact of debt. Understanding these metrics helps investors, analysts, and corporate finance professionals assess a company’s risk and make better investment decisions.