EBITDA vs. Cash Flow: Differences & Why It Matters

When analyzing a company’s financial performance, EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a commonly used metric. But is it the same as cash flow? How is it calculated? And does it always provide the full picture?

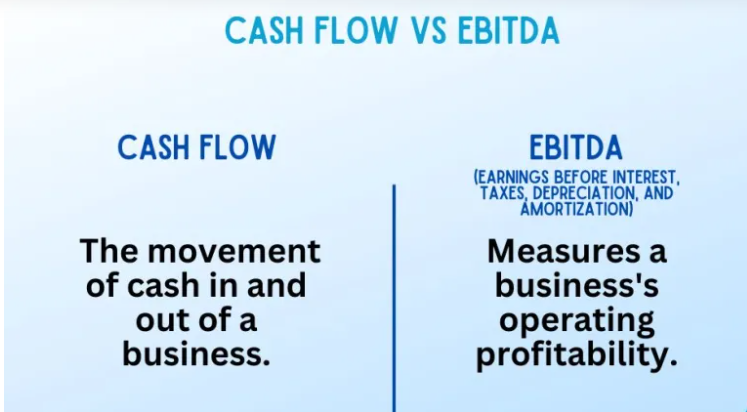

Is EBITDA the Same as Cash Flow?

No, EBITDA is not the same as cash flow. While both are used to assess financial health, they serve different purposes:

- EBITDA shows a company’s profitability before deducting interest, taxes, and non-cash expenses (depreciation & amortization).

- Cash Flow considers actual cash movements, including working capital changes, capital expenditures, and financing activities.

A company can have high EBITDA but low cash flow if it has significant capital expenditures or issues in collecting payments from customers.

How is EBITDA Calculated?

EBITDA is calculated using the following formula:

EBITDA=NetProfit+Interest+Taxes+Depreciation+Amortization

How Adjusted EBITDA Can Make Your Company More Attractive to Buyers

Adjusted EBITDA is a refined version of EBITDA that removes one-time, non-recurring, or unusual expenses. This gives potential investors a clearer picture of the company's true earnings potential.

What Adjustments Are Made?

- One-time legal or restructuring costs

- Owner’s personal expenses

- Unusual business losses or gains

- Non-recurring bonuses

By using Adjusted EBITDA, businesses can showcase a higher and more sustainable earnings figure, making them more appealing to investors or buyers.

When EBITDA is Just a Number

EBITDA is useful but not always reliable. It’s just a number when:

- The company has high debt, and interest costs are ignored.

- Capital-intensive businesses spend heavily on assets, which EBITDA overlooks.

- It doesn’t reflect actual cash available since it excludes working capital changes.

Investors should not rely on EBITDA alone but consider cash flow, net profit, and other financial metrics.

Limitations of EBITDA

While EBITDA is a popular metric, it has its flaws:

Ignores Debt & Interest Costs – Not useful for companies with heavy borrowing.

Excludes Capital Expenditures – Fails to show the real cash needed for business operations.

Not a Standardized Metric – Different companies may adjust EBITDA in different ways.

Can Be Manipulated – Companies can adjust EBITDA to inflate earnings.

Alternatives to EBITDA for Measuring Financial Performance

Since EBITDA has limitations, investors and analysts also use other metrics:

Operating Cash Flow (OCF) – Shows actual cash generated by business operations.

Free Cash Flow (FCF) – Measures cash available after capital expenditures.

Net Profit Margin – Indicates overall profitability after all expenses.

Return on Assets (ROA) & Return on Equity (ROE) – Measures efficiency in generating returns.

Each of these alternatives provides a more complete view of a company’s financial health than EBITDA alone.

Conclusion

EBITDA is a useful profitability metric, but it should not be confused with cash flow. While it helps in business valuation and investor decisions, it has several limitations. Relying only on EBITDA can be misleading, so businesses and investors should also consider cash flow, net income, and return ratios for a more accurate financial picture.